For many EB-5 investors, a loan can be an effective way to fund an investment while preserving liquidity and maintaining flexibility. Among the various financing options available, loans from privately owned companies have long been utilized by business owners and entrepreneurs seeking to qualify for the EB-5 program. While company loans remain a permissible source of EB-5 capital, recent adjudication trends suggest that USCIS is taking a closer look at these loans when reviewing Form I-526E petitions.

Although USCIS has not announced any formal policy changes targeting company loans, immigration attorneys and EB-5 practitioners have observed an increase in scrutiny from USCIS, including outright denials. As a result, investors considering a company loan should understand the heightened scrutiny that may accompany this funding strategy and ensure that their source of funds documentation is prepared accordingly.

The Legal Framework Has Not Changed

The good news for investors is that company loans remain an acceptable source of EB-5 investment capital. USCIS policy permits investors to use loan proceeds if the funds are obtained lawfully and the investor can demonstrate that they are personally and primarily liable for the debt. The agency’s focus remains on ensuring that the investment capital was lawfully sourced and that the transaction represents genuine indebtedness rather than a temporary transfer of funds.

In other words, the issue is not whether company loans are allowed—they are. The challenge lies in documenting the transaction in a way that satisfies USCIS’s increasingly detailed review standards.

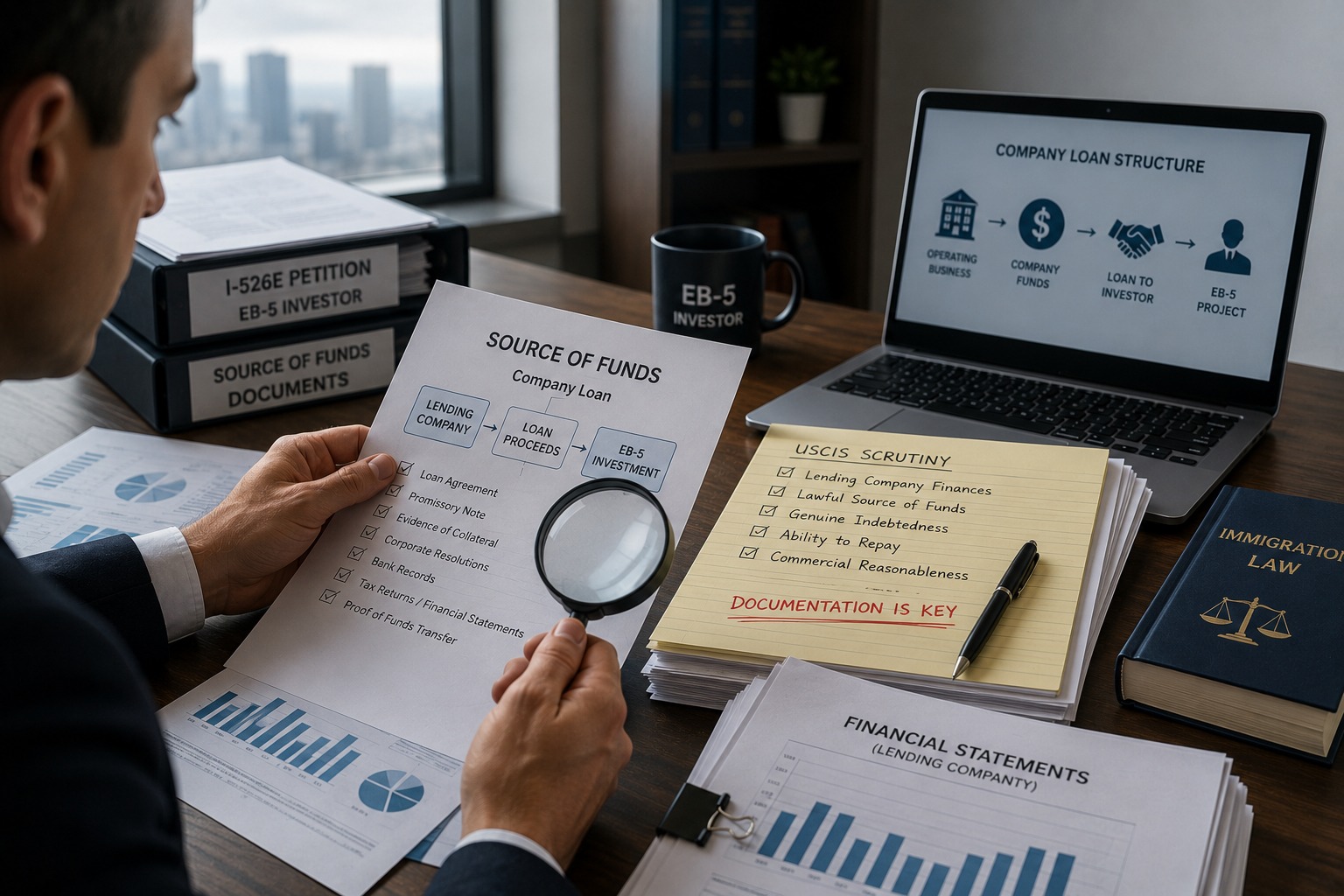

Why Company Loans Are Different from Traditional Bank Loans

When an investor obtains a loan from a major financial institution, USCIS often has less concern regarding the source of the funds. Banks are heavily regulated, and their ability to make loans is generally presumed.

Company loans are different. When a company, particularly a privately held business, provides the loan, USCIS may seek to understand where the company obtained the funds that were ultimately loaned to the investor. The agency may examine both the investor’s source of funds and the company’s source of funds.

This additional layer of review can significantly increase the amount of documentation required to support the petition.

Increased Focus on the Lending Company’s Finances

Recent activity indicates that USCIS officers are frequently requesting evidence demonstrating that the lending company had sufficient lawful funds available to make the loan. This can include corporate tax returns, audited financial statements, bank records, accounting reports, and documentation showing how the company generated its revenue.

The agency may also seek evidence that the company is a legitimate operating business and that the loan was made as part of a bona fide transaction rather than as a mechanism designed solely to facilitate an EB-5 investment.

For investors who own or control the lending company, this scrutiny can become even more extensive. USCIS may request corporate governance documents, shareholder resolutions, ownership records, and evidence establishing the investor’s authority to enter into the transaction on behalf of the company.

Closely Held Companies Face the Greatest Challenges

The most challenging cases often involve loans from closely held businesses or family-owned companies. In these situations, USCIS may closely examine whether the transaction reflects an arm’s-length loan and whether the terms are commercially reasonable.

Because the investor may have significant influence over the lender, adjudicators often seek additional assurances that the loan represents a genuine obligation to repay. Documentation showing loan terms, repayment schedules, interest provisions, collateral arrangements, and evidence of actual repayment activity can help demonstrate the legitimacy of the transaction.

USCIS may also inquire into whether the company had sufficient liquidity at the time the loan was issued and whether the loan was properly authorized under the company’s governing documents.

Documentation Is More Important Than Ever

Given current adjudication trends, investors should assume that a company loan will receive detailed review and prepare their source of funds package accordingly. A well-documented filing may include the loan agreement, promissory note, evidence of collateral, proof of fund transfers, corporate resolutions authorizing the transaction, financial statements, tax returns, and supporting evidence demonstrating the lawful source of the company’s assets.

The goal is to create a clear and transparent narrative that allows USCIS to trace the path of funds from the company’s lawful business activities through the loan transaction and ultimately into the EB-5 investment.

Planning Ahead Can Help Avoid Delays

One of the most common reasons company loan cases encounter difficulties is that investors wait until the I-526E filing process to begin gathering documentation. By that point, locating historical financial records, corporate approvals, and supporting evidence can be challenging and time-consuming.

Investors considering a company loan should work closely with experienced EB-5 counsel and source of funds professionals early in the process. Proper planning can help identify potential issues before filing and reduce the likelihood of receiving an RFE that could delay adjudication.

The above article is intended for informational purposes only. Anyone with specific issues relating to source of funds for an EB-5 petition should consult with an experienced immigration attorney.